All Categories

Featured

Table of Contents

[/image][=video]

[/video]

Surrender periods normally last 3 to 10 years. Since MYGA prices change daily, RetireGuide and its companions upgrade the complying with tables listed below frequently. It's important to check back for the most current info.

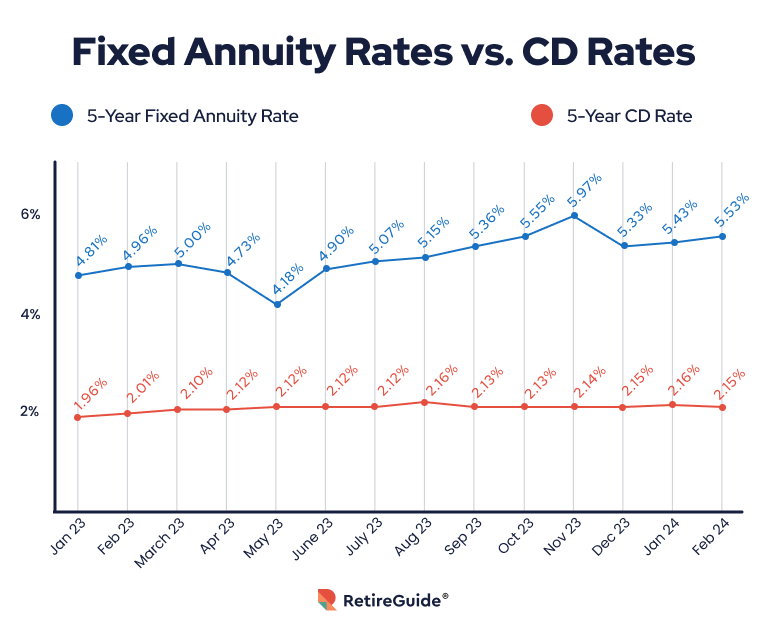

Several elements determine the rate you'll receive on an annuity. Annuity rates often tend to be higher when the general degree of all rate of interest rates is greater. When buying taken care of annuity rates, you might locate it valuable to compare rates to certifications of down payment (CDs), another prominent option for safe, trusted growth.

As a whole, set annuity prices surpass the prices for CDs of a comparable term. Apart from gaining a higher rate, a taken care of annuity might supply better returns than a CD since annuities have the benefit of tax-deferred development. This means you won't pay taxes on the rate of interest gained up until you begin getting repayments from the annuity, unlike CD interest, which is counted as gross income every year it's gained.

This led many specialists to think that the Fed would certainly reduce prices in 2024. Nonetheless, at a plan forum in April 2024, Federal Get chair Jerome Powell suggested that rates could not come down for some time. Powell said that the Fed isn't certain when rates of interest cuts may occur, as rising cost of living has yet to fall to the Fed's standard of 2%.

Pac Life Annuity Customer Service

Bear in mind that the most effective annuity rates today may be different tomorrow. It is very important to contact insurance coverage firms to verify their certain rates. Beginning with a free annuity appointment to find out just how annuities can assist fund your retirement.: Clicking will certainly take you to our companion Annuity.org. When contrasting annuity prices, it's vital to conduct your very own study and not only select an annuity just for its high rate.

Consider the kind of annuity. Each annuity type has a different series of average rate of interest. As an example, a 4-year set annuity might have a higher price than a 10-year multi-year guaranteed annuity (MYGA). This is because repaired annuities may supply a greater rate for the first year and afterwards reduce the price for the remainder of the term, while MYGAs ensure the price for the whole term.

The guarantee on an annuity is only as excellent as the firm that provides it. If the firm you purchase your annuity from goes broke or breast, you might lose money.

Annuity income rises with the age of the purchaser since the earnings will certainly be paid out in fewer years, according to the Social Security Management. Do not be amazed if your price is greater or less than someone else's, also if it coincides product. Annuity prices are simply one aspect to think about when purchasing an annuity.

Recognize the costs you'll need to pay to administer your annuity and if you need to cash it out. Cashing out can cost up to 10% of the worth of your annuity, according to the Wisconsin Office of the Commissioner of Insurance coverage. On the various other hand, administrative fees can add up over time.

Annuity Lawyers Near Me

Inflation Inflation can eat up your annuity's value over time. You can take into consideration an inflation-adjusted annuity that boosts the payouts over time.

Scan today's lists of the finest Multi-year Surefire Annuities - MYGAs (updated Thursday, 2025-03-06). For expert aid with multi-year ensured annuities call 800-872-6684 or click a 'Obtain My Quote' switch following to any kind of annuity in these lists.

You'll likewise enjoy tax obligation benefits that financial institution accounts and CDs don't offer. Yes. Most of the times deferred annuities enable a total up to be withdrawn penalty-free. However, the allowable withdrawal quantity can vary from company-to-company, so make certain to review the item sales brochure meticulously. Deferred annuities normally enable either penalty-free withdrawals of your gained interest, or penalty-free withdrawals of 10% of your agreement value each year.

The earlier in the annuity period, the higher the fine percentage, described as surrender charges. That's one reason it's ideal to stick to the annuity, once you commit to it. You can draw out whatever to reinvest it, yet before you do, make sure that you'll still triumph that method, even after you figure in the abandonment charge.

The surrender charge can be as high as 10% if you surrender your agreement in the initial year. An abandonment charge would be charged to any withdrawal greater than the penalty-free quantity permitted by your deferred annuity contract.

You can set up "methodical withdrawals" from your annuity. Your various other alternative is to "annuitize" your deferred annuity.

What Is A Qualified Joint And Survivor Annuity

This opens a variety of payment choices, such as earnings over a solitary life time, joint lifetime, or for a specific duration of years. Several postponed annuities permit you to annuitize your agreement after the first agreement year. A major distinction remains in the tax obligation treatment of these products. Rate of interest made on CDs is taxed at the end of yearly (unless the CD is held within tax obligation professional account like an individual retirement account).

The interest is not taxed up until it is removed from the annuity. In other words, your annuity expands tax obligation deferred and the interest is intensified each year.

Fng Annuity

You have numerous alternatives. Either you take your money in a swelling sum, reinvest it in one more annuity, or you can annuitize your agreement, transforming the swelling sum into a stream of earnings. By annuitizing, you will just pay taxes on the rate of interest you obtain in each payment. You have 30 days to notify the insurance policy company of your intents.

These functions can vary from company-to-company, so be sure to discover your annuity's fatality benefit attributes. With a CD, the interest you make is taxed when you make it, also though you don't receive it until the CD matures.

So at the very least, you pay tax obligations later, as opposed to earlier. Not only that, yet the intensifying rate of interest will be based upon an amount that has not currently been strained. 2. Your recipients will get the full account worth as of the day you dieand no surrender charges will be deducted.

Your recipients can choose either to obtain the payout in a round figure, or in a series of income settlements. 3. Commonly, when somebody passes away, even if he left a will, a court decides that obtains what from the estate as occasionally family members will certainly suggest about what the will methods.

It can be a long, made complex, and really pricey procedure. People go to wonderful lengths to prevent it. However with a multi-year fixed annuity, the owner has plainly marked a recipient, so no probate is needed. The cash goes directly to the recipient, no doubt asked. If you contribute to an individual retirement account or a 401(k) plan, you obtain tax deferral on the incomes, similar to a MYGA.

{kind=link}

Table of Contents

Latest Posts

Reliance Annuity

Schwab Variable Annuity

Ubs Annuities

More

Latest Posts

Reliance Annuity

Schwab Variable Annuity

Ubs Annuities